Auto Insurance in Greeley, CO — Your Neighbors, Your Advocates

From I-25 winter ice to hailstorms that shut down the city, Greeley drivers face unique risks. Get coverage built for northern Colorado roads—at prices that fit your family budget. We're local, we get it, and we make insurance simple.

✓ No obligation • ✓ Takes 3 minutes • ✓ Compare 20+ carriers

Why Greeley Families Choose JWR for Auto Insurance

We're not just selling policies—we're protecting neighbors.

WE KNOW GREELEY ROADS

Family-owned and serving northern Colorado for over 20 years. We know the I-25 corridor accidents, the summer hailstorms, the winter black ice on 34th Avenue, the University of Northern Colorado student drivers. We're not a call center in another state—we're right here in your community.

WE SPEAK PLAIN ENGLISH

No insurance jargon. No fine print surprises. We explain coverage options like you're sitting at our kitchen table—because that's how we'd want to be treated. You'll actually understand what you're buying.

WE SHOP 20+ CARRIERS FOR YOU

Why settle for one option? We compare rates and coverage from top carriers so you get the best value for your situation. One call, multiple quotes. Whether you're a UNC student, JBS employee, or young family, we find what fits.

Real Situations, Real Protection for Greeley Drivers

Here's what auto insurance actually covers when life happens on northern Colorado roads

10TH STREET / 23RD AVENUE INTERSECTION

Greeley's busiest east-west corridor sees a couple of crashes a week at the 23rd Avenue light. Late afternoon, you're stopped at the red and a driver coming off US-85 doesn't slow in time. Rear-end at 30 mph, $9,800 in damage to the back of your truck, plus four weeks of physical therapy on a soft-tissue injury. Your collision pays the truck repairs immediately; medical-payments coverage on your auto policy pays the PT bills regardless of fault. Without medpay, the bills sit on your tab until the at-fault driver's carrier finally settles — typically six to nine months on a Greeley urban-corridor claim.

MAY 28, 2024 — THE GREELEY HAILSTORM

A foot of hail across east Greeley. Stones up to baseball-size shattered windshields, totaled hundreds of vehicles, and produced $1.45 million in municipal damage alone. Private vehicle claims ran into the tens of millions. Comprehensive coverage with a reasonable deductible (≤$1,000) is the line that totaled vehicles and paid the new ones; collision did nothing here. If you parked uncovered anywhere from the JBS plant to the UNC campus that afternoon, you found out which line your policy actually had. Greeley sits in one of the highest-frequency hail markets in the lower 48 — this is not insurance for a once-a-decade event.

UNINSURED DRIVER ON HIGHWAY 34

Highway 34 east of Greeley moves freight, agricultural traffic, and oil-pad service trucks alongside daily commuters. A driver running on an expired plate without insurance crosses the centerline near LaSalle and clips your driver's side, totaling the car. Their carrier? They don't have one. Uninsured-motorist coverage is what pays your medical bills, your lost wages, and the difference between what your collision pays out and what your car was actually worth. Roughly one in six Colorado drivers is uninsured or underinsured. UM/UIM is the cheapest meaningful coverage on a Greeley policy.

What Does Auto Insurance Actually Cover?

Let's cut through the confusion—here's what each type of coverage actually does for you in Greeley

COMMON MYTHS ABOUT AUTO INSURANCE

Myth: "My insurance follows me when I drive someone else's car."

Truth: Insurance follows the vehicle, not the driver. If you borrow a friend's car and crash, their insurance pays first.

Myth: "Comprehensive coverage means it covers everything."

Truth: Comprehensive covers non-collision events (hail, theft, deer). It doesn't cover collisions—that's separate collision coverage.

Myth: "My insurance covers me when I drive for Uber or DoorDash."

Truth: Personal auto policies exclude commercial use. You need rideshare coverage—we can add it for about $10-$20 monthly.

Myth: "Red cars cost more to insure."

Truth: Vehicle color doesn't affect rates. Make, model, age, safety ratings, and repair costs matter—not paint color.

Myth: "Colorado minimum coverage is enough."

Truth: State minimums ($25K/$50K) won't cover serious accidents. Most Greeley families need $100K/$300K to protect assets.

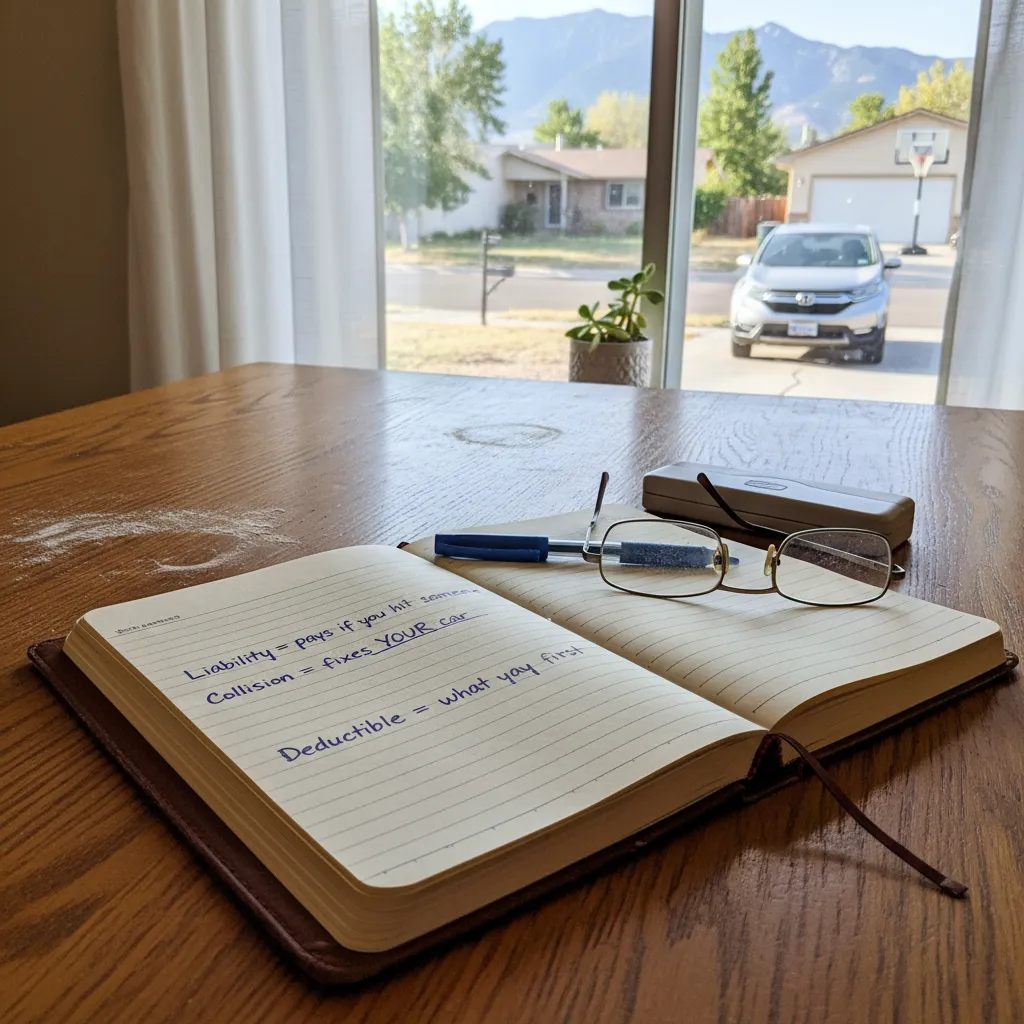

WHAT YOUR AUTO INSURANCE COVERS

- Liability Coverage: Pays for injuries and property damage you cause to others (required by Colorado law—minimum $25,000 per person, $50,000 per accident)

- Collision Coverage: Repairs your vehicle after accidents with other cars or objects, regardless of fault

- Comprehensive Coverage: Covers hail damage, theft, vandalism, deer strikes, and weather events (critical in Greeley's hail corridor)

- Uninsured Motorist: Protects you when hit by drivers with no insurance or insufficient coverage

- Medical Payments: Covers medical bills for you and passengers regardless of fault

- Rental Reimbursement: Pays for rental car while yours is being repaired ($30-$50 daily)

- Roadside Assistance: 24/7 towing, flat tire service, lockout help, fuel delivery

- Gap Insurance: Covers difference between loan balance and vehicle value if totaled

Ready to Protect Your Greeley Vehicle?

Get your free quote in 3 minutes—compare 20+ carriers for northern Colorado families

Which Coverage Option Is Right for You?

Here's how to figure out what works for your situation. What do you need?

Roadside Assistance for Auto Insurance

From Wyoming interstates to Colorado mountain passes, vehicle breakdowns happen when you least expect them—flat tires on remote highways, dead batteries in subzero temperatures, lockouts in grocery store parking lots, and mechanical failures far from home. As an independent brokerage serving Wyoming, Colorado, Utah, and Montana, we compare 20+ carriers to find roadside assistance coverage that actually helps when you're stranded—with towing to your preferred shop, jump-starts in brutal winter conditions, and service that reaches rural areas where national programs often won't dispatch. We're locals who've been stuck on these same roads, and we make sure your roadside coverage works when you need it most—not just looks good on paper.

Uninsured/Underinsured Motorist for Auto Insurance

Even in Wyoming, where only 5.9% of drivers lack insurance—the nation's lowest rate—one in seventeen vehicles on the road has no coverage to pay you if they cause an accident, leaving you facing medical bills, lost wages, and pain-and-suffering damages with nowhere to turn. As an independent brokerage serving Wyoming, Colorado, Utah, and Montana, we compare 20+ carriers to structure uninsured and underinsured motorist coverage that protects YOUR family when at-fault drivers have no insurance or inadequate limits—ensuring serious accidents don't become financial catastrophes because someone else failed to maintain proper coverage. We're local experts who answer the phone, explain coverage gaps in plain English, and make sure you're protected from the devastating consequences of being hit by uninsured or underinsured drivers on Mountain West roads.

Medical Payments Coverage for Auto Insurance

When accidents happen on Wyoming roads or Colorado highways, you need immediate medical care—not weeks of waiting while insurance companies determine fault. As an independent brokerage serving Wyoming, Colorado, Utah, and Montana, we compare 20+ carriers to find Medical Payments Coverage that covers your medical bills from the first dollar—no deductibles, no co-pays, no fault determination required—protecting you and your passengers when accidents happen. We're local experts who answer the phone, explain how MedPay works in plain English, and make sure you're not stuck paying thousands out of pocket while waiting for liability claims to process.

Comprehensive Coverage for Auto Insurance

We understand driving in the Mountain West—from Wyoming hail storms to Colorado mountain roads. As an independent brokerage with 20+ carriers, we find the right comprehensive auto coverage for your vehicle and lifestyle, with honest local expertise and no pressure.

Collision Coverage for Auto Insurance

Mountain West drivers face unique collision risks—from icy Wyoming highways where winter crashes spike, to hail-damaged Colorado roads with debris, to remote Utah routes where hitting stationary objects means costly repairs far from help. As an independent brokerage serving Wyoming, Colorado, Utah, and Montana, we compare 20+ carriers to find collision coverage that actually protects YOUR vehicle when accidents happen—whether you're at fault, hit by an uninsured driver, or involved in a hit-and-run. We're local experts who answer the phone, explain deductibles and coverage limits in plain English, and make sure your vehicle investment is protected from the collision risks that threaten Mountain West drivers every day.

Liability Coverage for Auto Insurance

Mountain West drivers face unique liability risks—from devastating multi-vehicle pileups on icy Wyoming highways to rear-end collisions in Fort Collins traffic to accidents on remote Utah roads where medical transport costs skyrocket. As an independent brokerage serving Wyoming, Colorado, Utah, and Montana, we compare 20+ carriers to find auto liability coverage that actually protects YOUR assets when you're at fault—with limits high enough to prevent lawsuits from draining your savings, home equity, and retirement accounts. We're local experts who answer the phone, explain liability limits in plain English, and make sure an at-fault accident doesn't destroy everything you've built.

Do You Actually Need Auto Insurance?

YOU DEFINITELY NEED AUTO INSURANCE IF:

- ✓ You own or lease any vehicle registered in Colorado (it's the law)

- ✓ You commute on I-25 between Greeley and Denver or Fort Collins

- ✓ You can't afford to replace your vehicle from savings if totaled

- ✓ You park outside in Greeley's hail corridor (May-August risk)

- ✓ You have teenage drivers or University of Northern Colorado students on your policy

- ✓ You drive through winter conditions on Colorado roads

- ✓ You have assets to protect from liability lawsuits (home, savings, retirement)

- ✓ You drive for work, rideshare, or delivery (need specialized coverage)

- ✓ You're financing or leasing (lenders require comprehensive and collision)

- ✓ You drive Highway 34 to Estes Park or mountain roads (deer strikes common)

SPECIAL SITUATIONS IN GREELEY:

→ UNC students

Ask about student discounts and good student rate reductions (up to 25% off)

→ JBS USA employees

Inquire about workplace affinity programs and group discount opportunities

→ Rideshare or delivery drivers

Must add commercial or rideshare endorsement—personal policies exclude business use

→ Multi-vehicle households

Bundle all vehicles for 20-30% multi-car discounts

→ Homeowners

Bundle auto + home for 15-25% savings and simplified claims

→ Long-distance I-25 commuters

Consider higher liability limits and comprehensive coverage for increased exposure

→ Classic car enthusiasts

Ask about specialized classic/collector vehicle insurance (often cheaper than standard policies)

STEP 1: UNDERSTAND COLORADO REQUIREMENTS

Colorado mandates minimum liability ($25K per person, $50K per accident, $15K property damage). But is that enough? Consider what you'd lose in a serious accident. Most Greeley families need $100K/$300K liability to truly protect assets.

If financing or leasing, your lender requires comprehensive and collision coverage—that's non-negotiable.

STEP 2: ASSESS YOUR GREELEY RISKS

Do you park outside during hail season (May-August)? Commute on I-25 during winter? Drive through deer-heavy areas on Highway 34? Have teenage drivers?

High-risk situations need comprehensive coverage, uninsured motorist protection, and higher liability limits.

STEP 3: CALCULATE YOUR FINANCIAL EXPOSURE

Could you replace your vehicle from savings if totaled tomorrow? Pay $100K in medical bills if you cause serious injuries? Cover rental car costs during repairs?

Your coverage limits should reflect what you can't afford to lose.

STEP 4: COMPARE BUNDLING SAVINGS

If you own or rent in Greeley, bundling auto + home/renters typically saves 15-25%. Add life insurance and save even more.

We'll show you exact savings across 20+ carriers.

STEP 5: TALK TO US

Not sure what fits your Greeley situation? Call us at (970) 401-8140. We'll walk you through it—no pressure, just honest advice from neighbors who know northern Colorado roads.

Ready to Get the Coverage You Deserve?

Get your free quote in 3 minutes, or call and we'll handle it together.

FAQs

Auto insurance is legally required in both Wyoming and Colorado. While the minimum liability limits might seem low, they often aren't enough to cover serious accidents. Driving without insurance can lead to hefty fines, license suspension, and personal financial responsibility for all damages if you're at fault in a crash. It's not just optional; it protects you and others.

Liability-only insurance covers damages and injuries you cause to other people and their property. "Full coverage" typically adds collision and comprehensive coverage, protecting your own vehicle from accidents, theft, or natural disasters like a Wyoming hailstorm. If you have a newer car, an auto loan, or want maximum protection, full coverage is often recommended. For older vehicles, liability-only might suffice, but consider the financial risk.

Auto insurance premiums in Wyoming and Colorado can vary widely, often ranging from $100 to $250 per month depending on factors like your driving record, vehicle type, and coverage limits. For example, a driver with a clean record in Cheyenne will likely pay less than someone with an accident history in Denver, especially if they commute through oil fields. The best way to know your exact cost is to get a personalized quote.

After ensuring everyone's safety and, if necessary, contacting law enforcement, you should report the accident to your insurance provider as soon as possible. We'll guide you through gathering necessary information, documenting damages, and working with an adjuster to assess your claim. Timely reporting helps expedite the process, getting you back on the road sooner.

A comprehensive auto policy typically includes liability coverage for damage to others, collision coverage for your vehicle in an accident, and comprehensive coverage for non-collision events like hail damage, falling rocks, or wildlife collisions common in Wyoming and Colorado. Many policies also include medical payments and uninsured motorist coverage, which is crucial given the higher rates of uninsured drivers in some areas.

Standard auto insurance generally does not cover intentional damage, normal wear and tear on your vehicle, or modifications and custom parts not explicitly declared on your policy. It also won't cover using your personal vehicle for racing or certain commercial purposes like ridesharing without specific endorsements. Always check your policy for precise exclusions.